RAI and LUSD: Stablecoins Built for Resilience

Breaking down the two top options for decentralized stables

How do you explain this transaction??

Someone recently swapped just over half a million DAI for under 490k LUSD, both stablecoins with a $1 peg. However, despite the nominal difference between these amounts, the value of the LUSD received equals the value of the DAI sold, minus small amounts of fees and slippage. This means LUSD must be trading above its intended peg, at least at the time of the swap. There’s no money to be made for the DAI seller here, assuming LUSD will revert to its peg which it’s well designed to do. So the question remains, why execute a massive stablecoin swap where you stand to make no money and potentially lose up to $12k?

The answer: this person is willing to pay a premium for a stablecoin with a decentralized and robust design, and in the face of wallet blacklists, government sanctions, and failed stablecoin experiments they’re not the only ones. Herein we’ll look at two of the most promising decentralized stablecoins on the market today, RAI and LUSD.

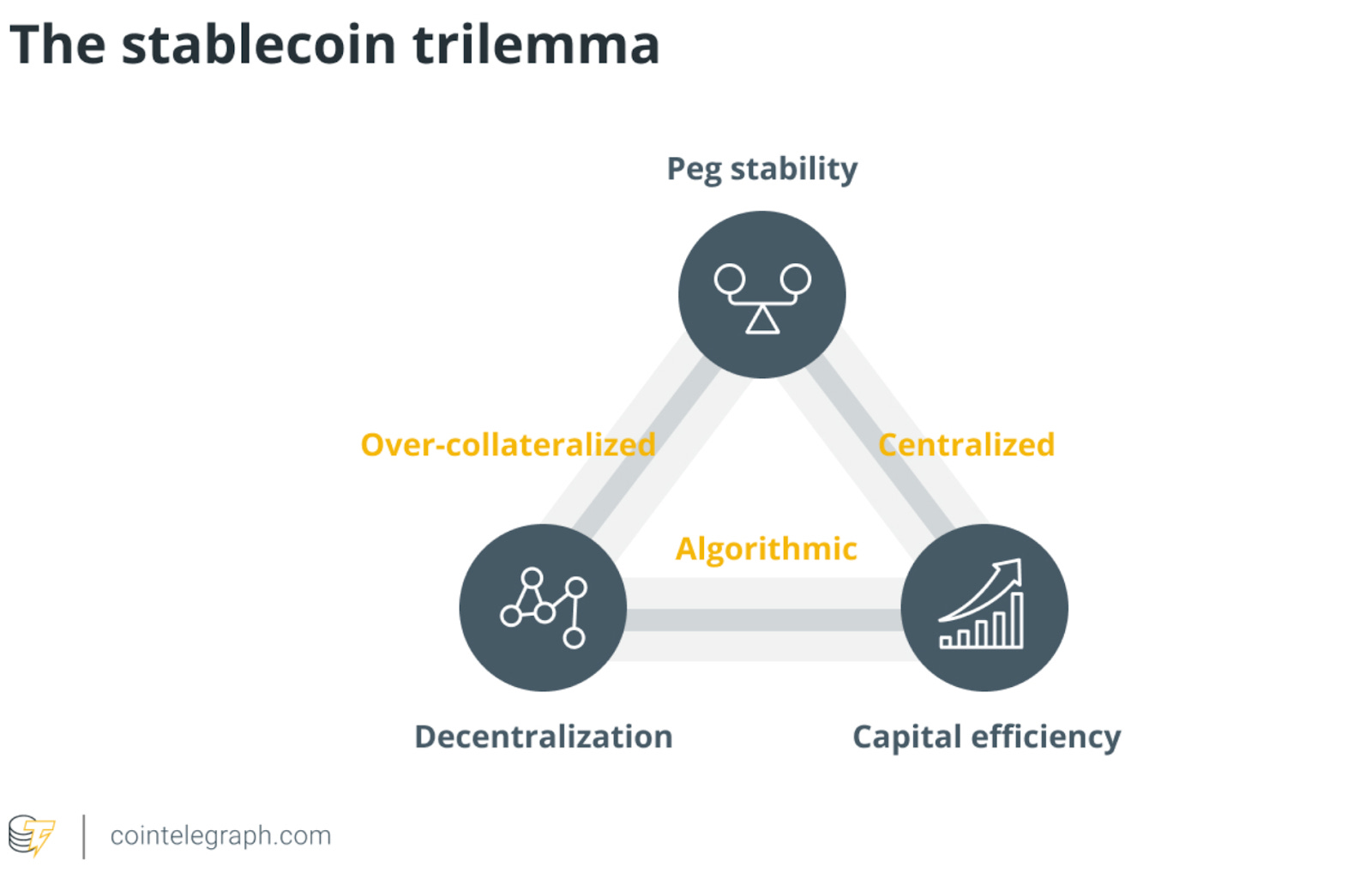

Tackling the Trilemma

So what exactly is the case for ETH backed stablecoins? Like blockchains and international monetary policy there exists a trilemma within stables. The three trade offs involved are decentralization, stability, and capital efficiency. Scalability is another factor to consider, but I’d argue that it’s a secondary consideration, as it makes no sense to scale something that doesn’t serve its intended purpose, and scalability is also a component of capital efficiency.

Decentralization: Not backed or controlled by any centralized entity, this is the component sacrificed by all fiat reserve stablecoins like USDC, USDT, and to some extent DAI.

Stability: Strong mechanisms in place to maintain the intended peg and minimize volatility, this is where most algorithmic stablecoins like Terra’s UST have failed as they rely on demand for an unbacked pair asset like LUNA.

Capital Efficiency: The collateral ratio required to mint a stablecoin, this is another issue with coins like DAI, which requires 150% collateralization, limiting the efficiency.

The teams at Liquity and Reflexer Labs both have made significant progress on the stablecoin trilemma, providing the market with reliably backed and decentralized stables without excessive collateral requirements. There are quite a few similarities between the two projects, such as the shared Ethereum-only backing and a minimal/zero governance philosophy. However, the mechanisms and overall approach used to achieve stability vary significantly, and it’s worth taking a look at each separately to understand why RAI and LUSD are constructed as they are.

Liquity and LUSD

Starting off with Liquity, we have a protocol that allows users to create collateralized debt positions (CDP) by depositing ETH to a “trove” where it is locked in exchange for LUSD, a stablecoin that holds its value by always being redeemable for $1 worth of ETH within the protocol. Users are able to mint LUSD up to 91% of their collateral value, and pay no interest on the loan, both incredibly borrower friendly features.

The only fees involved are a floating redemption and borrow fee, which ranges between .5% and 5% percent and is incurred when LUSD is minted or burned. This rate is one of the key mechanisms for maintaining LUSD price stability, raising redemption fees when LUSD is above its peg, and raising borrowing fees when below the peg. This fee will then decay over time as LUSD supply and demand levels out, so it usually remains relatively low, but this mechanism does limit capital efficiency at scale. Fees then accrue to stakers of LQTY, the protocol’s non pegged token. When you think Liquity, think capital efficiency, especially when it comes to mid-long term borrowing, due to the 0% interest, low total fees, and favorable minimum collateral ratio.

One interesting aspect of LUSD is that it often trades slightly above its $1 peg, which is why it’s referred to as a soft peg, in the range between $1.00 and $1.10. Inside this range there is no directional incentive to either mint or burn LUSD due to the MCR of 110%, so it can float around based on overall supply and demand. Outside of this range an arbitrage opportunity is presented that establishes a hard peg, as it becomes profitable to either market buy LUSD under $1 and redeem it for ETH, or max mint LUSD with ETH and market sell when it trades over $1.10. This arb, along with the floating redemption/borrow rate, maintains LUSD’s dollar peg without the need for fiat currency reserves. This can be seen as a negative since LUSD will often remain above $1.00 for extended periods of time, and if you need to purchase LUSD to pay back a debt position you could very well be paying over $1 on the open market. I’d argue it’s a reasonable tradeoff for the diminished risks and low collateral ratio, but certainly something to consider when opening a trove.

Redemptions, Liquidations, and Cheap ETH

Some other features that make Liquity unique are the redemption process and Stability Pool, which are in place to maintain solvency within the protocol. When you redeem LUSD for ETH on Liquity you’re not paying down your own debt position. Rather, you’re paying down the debt of the troves at risk of falling below the MCR, and receiving an equal amount of those troves’ ETH minus the redemption fee. In order to avoid being redeemed against trove owners can add additional collateral to keep their position above the MCR, but being redeemed against doesn’t result in any real loss as a trove’s debt is canceled equivalently to the amount of the collateral they lose.

When a trove does fall below the MCR it becomes eligible for liquidation, and then the Stability Pool comes into play. This is a pool full of staked LUSD which absorbs liquidations by burning an amount equivalent to the debt of a liquidated trove. In return the stakers receive the trove’s collateral proportional to their stake in the pool. Since troves are overcollateralized and typically liquidated just under the MCR, liquidations create positive value for pool participants effectively allowing them to buy cheap ETH.

On top of all this, Liquity is entirely immutable as a protocol, meaning all the smart contracts that carry out its functions are unable to be upgraded and no governance mechanisms exist to alter its parameters. Overall it scores highly for all three of the trilemma conditions, and is being adopted by a growing number of protocols and DAOs across Ethereum and its L2s which we’ll touch on more after diving into RAI.

Reflexer and RAI

RAI is based on the original concept of MakerDAO’s DAI, before it expanded to its current state involving multiple sources of collateral. It’s another CDP based stablecoin and like LUSD can only be minted with ETH collateral. It’s MCR is substantially higher at 135%, meaning you can borrow up to 74% of your collateral value in RAI. Borrowing fees are relatively low with a 2% annual “stability fee”, so compared to LUSD this could be higher or lower than what rate you get on borrow/redemption it depends on timing. Where RAI starts to really differentiate is the price, which is not dollar pegged and typically ranges from $2.80 - $3.20, as well as the mechanics behind how volatility is managed.

The Money God

That’s what Reflexer calls its algorithmic controller, which works in basically the same way as modern monetary policy, by controlling interest rates. The controller observes the difference between RAI’s market price and its redemption value, then adjusts the redemption rate to incentivize a convergence of those two prices. The market price is observed via Chainlink oracles from major dexes like Curve, and the redemption price is internal to the Reflexer protocol, dictating how much ETH you get when redeeming one RAI. There’s basically two scenarios that can occur:

If market price > redemption price the redemption rate is decreased- holders are incentivized to lend out RAI- pushing the market price down

If market price < redemption price then the redemption rate is increased- holders are incentivized to pay back borrowed RAI- pushing the market price up

The controller also considers historical price deviations when making adjustments in order to help size the changes appropriately.

As you can see here there is not a target price for RAI besides keeping the RP and MP aligned, so it’s considered a floating stablecoin as opposed to a pegged stable like LUSD or DAI. The purpose behind this is to maintain a steady real value as RAI is not subjected to the effects of US monetary policy via a dollar peg. Take the current Fed regime for example, where years of printing has devalued the dollar and put inflation rates at a lofty 8%. Dollar pegged stables are a claim to $1 worth of their backing assets, so over a long enough time frame the dollar depreciating against those assets will erode real redemption value. In this sense it can be argued that RAI is more decentralized than other stables, as no centralized entity can affect its value.

Liquidations and Governance

When it comes to liquidations, users have a one hour buffer after their collateral ratio falls below the minimum 135% and Keeper bots conduct the liquidation through an auction process. Once the collateral is sold and the debt is covered, Reflexer takes a cut of any that is left over up to 10% of the liquidated safe’s original debt amount. This liquidation penalty fee accrues to stakers of Reflexer’s governance/utility token FLX, and if there is any collateral left afterward the debt and penalty are covered the user who’s safe was liquidated can claim it back. Reflexer does offer a sort of insurance mechanism on deposits called the Savior. Activating this insurance involves depositing a RAI/ETH Uniswap v2 LP token to the safe, which is used to top up collateral if the liquidation threshold is ever reached.

Currently RAI does have a governance process where proposals can be voted on by holders of the FLX token. This allows for alterations of protocol parameters such as the MCR, stability fee, and minimum deposit amount. In the past, governance has lowered the MCR from 145% to the current 135%, and the minimum deposit amount started out at 800 RAI, but is currently at considerably high 3149 RAI. The ultimate goal of Reflexer is to minimize governance, for all the same reasons as Liquity has removed the mechanism entirely, but for now a small amount of governance risk remains.

Trilemma Analysis

For Reflexer, decentralization is the most valued trait of the three and it's not even close. Taking the idea of an ETH backed stablecoin to the next level by removing the dollar peg is what sets RAI apart. Stability is the second highest priority, as the price is allowed to float and has seen some action over its history, but in general volatility is tamped down by the Money God algorithm. The case could even be made that over the long term this system will provide more real price stability due to insulation from U.S. monetary policy. As for capital efficiency, RAI is relatively poor compared to LUSD, but is still better than DAI. I’d assume the fact that the project originated from the idea behind single collateral DAI contributes to the more conservative minimum collateral ratio. This also raises the topic of scalability, as RAI usage is still relatively low compared to other stablecoins. The willingness of potential users to accept this inefficiency as well as the complexity of the system is yet to truly be seen.

Vitalik on RAI

The Ethereum cofounder has been a public supporter of Reflexer’s work for a while now, coming out with a blog post after the Terra collapse which highlighted RAI as an “ideal” stablecoin. His logic is that RAI’s reliance on an exterior asset (ETH) as opposed to an asset internal to the system (Terra’s LUNA) would allow it to function properly even during a period of rapidly decreasing demand for RAI. He also highlights the value of integrating negative interest rates as a means of maintaining real price stability, contrary to dollar pegged stables which are exposed to USD inflation.

In his latest blog post tackling the state of DAOs and the role of governance, Buterin posits that stablecoins don’t need to be efficient, only stable and decentralized. He also expands on the argument against dollar pegging, proposing a scenario in which hyperinflation makes it an unreliable asset to use as a peg and stablecoins must switch to an on-chain CPI calculation to track instead. This of course would require a governance mechanism to carry out, and would present an issue to Liquity as the protocol is fully immutable. Later on in the post he highlights a scalability issue pertinent to RAI, where issuing more debt than the market cap of their governance token FLX could bring about a scenario where it becomes profitable to amass a controlling stake in order to manipulate price feeds and liquidate borrowers.

Vitalik makes some solid points about tail risks, but my intended purpose for this post isn’t to say either LUSD or RAI is a superior option. This is to outline the design differences as well as the reasoning behind them and the effects they create. Protocols and DAOs are adopting both instead of fiat back stablecoins, and the choice ultimately comes down to user preferences between the trilemma components.

The Decentralization Premium

Now at this point that swap which was highlighted at the beginning should make more sense. A growing number of protocols, DAOs, and individual DeFi participants are realizing the benefits of ETH backed stablecoins and making the switch. Obviously decentralization is the main factor here with censorship from the two main centralized stables, USDC and USDT, being the main element of risk. Their history of asset freezing has contaminated DAI as well, since it is backed by over 50% USDC.

Censorship directly opposes the ethos of DeFi, and is a big reason why protocols like Synthetix have phased DAI out of their treasuries, in their case opting for LUSD instead as a reserve asset to back their own sUSD stablecoin. RAI is being similarly adopted, with the likes of GnosisDAO and Frax holding it as a treasury asset. If we do see a continued increase in blacklisting, the good news is LUSD and RAI will be fully insulated, and likely see a surge in demand as safer options. Both are decently equipped to handle a large influx of capital, but the floating fees and rates in play would limit how fast money can enter either system by increasing the premium to be paid.

On the topic of regulatory risk, which we’ve seen rear its head recently with the OFAC sanctions placed on TornadoCash, there’s not much clarity at the moment as to the fate of stablecoins. In my opinion it would be absurd to expect the same sort of treatment for RAI, LUSD, DAI or any other stable. Conducting illegal activities such as money laundering on-chain is extremely traceable, save unique cases like TornadoCash where the protocol offers anonymity as a feature. That being said, the Terra collapse did attract the attention of regulators to stablecoins, and algorithmic ones in particular. Earlier this week there were reports from Bloomberg concerning a stablecoin related draft bill circulating in the U.S. House of Representatives, which allegedly contains a two year ban on algo-stables.

The key word here is endogenously, meaning the collateral originates from the same source as the stablecoin. It would appear this distinction exempts ETH collateralized stables since protocols like LUSD and RAI have no influence over ETH supply. This news and potential enactment of such a ban would likely push holders of any Terra style stables- Tron’s USDD comes to mind- into unaffected ones.

In Summary

ETH backed stablecoins are the best bet we have right now for a truly decentralized option. While LUSD and RAI have different tradeoffs between levels of decentralization, stability, and capital efficiency, both are strong options in the face of blacklists and looming regulations. That isn’t to say these stables are risk free, as factors like governance, oracle dependence, and dollar devaluation are important to consider. Overall, both have proven to be resilient in a variety of market environments and supply/demand conditions, making them some of the best options for treasury assets as well as acquiring leverage on held ETH.

Enjoyed the read. A couple of questions

1. With the RAI protocol, is there a point that the redemption rate drops to zero to encourage reduction in supply and it is still not enough. You mentioned -ve interest rates as the incentive?

2. I note the price of RAI has trended downwards over the last few months. What's to explain that. Is that just it following the price of eth? If so aren't you just being indirectly exposed to eth which defeats the whole process of a stable coin which is to keep its price stable